A Beginner’s Guide to Autocallable ETFs: Earning Income from the Stock Market

Income investing has always involved a trade-off between yield and risk. Bonds offer stability but modest returns. Dividend stocks offer income but full equity exposure. A newer category of structured investment — the autocallable note — sits in a different part of that spectrum: higher income potential than most fixed-income options, with a clearly defined set of equity-linked risks.

Until recently, autocallable notes were only available to institutional investors and high-net-worth clients through private banks. That’s changing. A new generation of autocallable ETFs is bringing this strategy to a much broader audience — and changing what income investing can look like in a diversified portfolio.

What Are Autocallable Notes?

An autocallable note is a structured, market-linked debt instrument that pays a regular coupon — typically monthly — as long as a reference index stays above a predefined level. If the index performs strongly enough, the note redeems early and returns principal ahead of its scheduled maturity date. If the index falls sharply and stays down, income can be interrupted and principal can be at risk.

The reference index is usually a broad equity benchmark — the S&P 500, the Nasdaq-100, or in the case of ATCL, the Bloomberg US Large Cap VolMax Index, a volatility-targeted version of the 500 largest U.S. companies. The performance of that index relative to a set of predefined thresholds determines everything: whether a coupon gets paid, whether the note gets called early, and whether principal is returned in full at maturity.

The appeal is straightforward: autocallable coupons are typically well above what investment-grade bonds offer, because investors are compensating for equity-linked downside risk rather than just credit or duration risk. The income is higher because the trade-off is different — not better or worse, just different.

How Autocallable Notes Work: The Key Structural Terms

Every autocallable is defined by a small set of parameters. Understanding these is essential to understanding what you own.

The Coupon Barrier

The index level below which monthly income stops. In ATCL, this is set at 60% of the initial index level — meaning the market would need to fall more than 40% before coupons are interrupted. If the index closes above this barrier on a monthly observation date, the coupon is paid. If it closes below, that month’s payment is skipped and cannot be made up later. Autocallable income is contingent, not guaranteed.

The Autocall Barrier

The level at which the note redeems early. In ATCL, set at 100% of the initial index level and checked monthly after a one-year non-call period. If the index is at or above its starting value, the note is automatically called — investors receive full principal plus that month’s coupon, and the note ends.

The Non-Call Period

An initial window — one year in ATCL — during which early redemption cannot happen even if the index is above the autocall barrier. This gives the strategy time to generate income before potentially being called away in a rising market.

The Maturity Barrier

If a note is never called, it runs to final maturity — typically five years. The maturity barrier determines principal treatment. In ATCL, this is set at 50% of the initial index level. If the index finishes above that level, investors receive full principal. If below, principal is reduced 1-to-1 with the index’s loss from its starting level. For example: a 55% index decline on a note with a 50% maturity barrier would return 45 cents on the dollar.

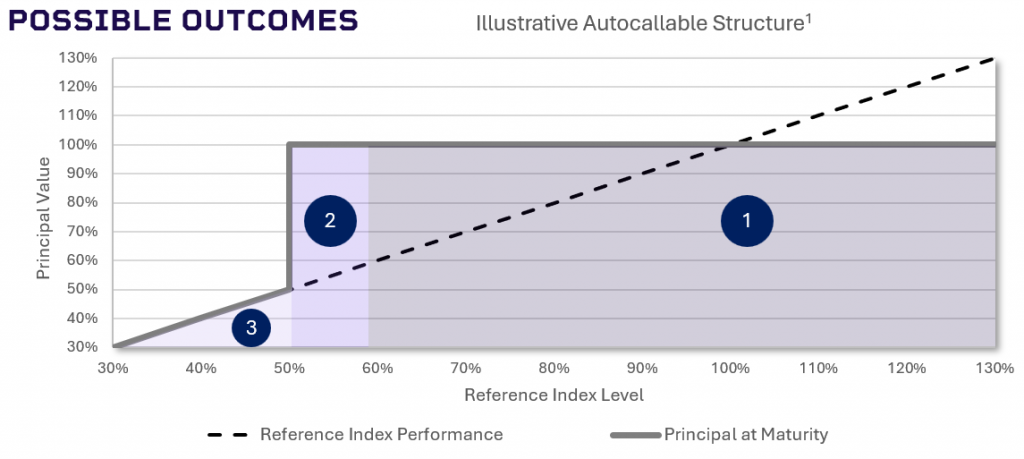

The Three Outcome Scenarios

Regardless of what happens in between, autocallable notes resolve into one of three broad outcomes depending on where the index finishes on its observation dates.

For illustrative purposes only. Assumes a representative autocallable with a 60% coupon barrier, 50% maturity barrier, and monthly observation periods. After 1-year non-call period, autocallables will return principal if reference index positively breaches 100% at any observation date.