Examining the ETF Landscape

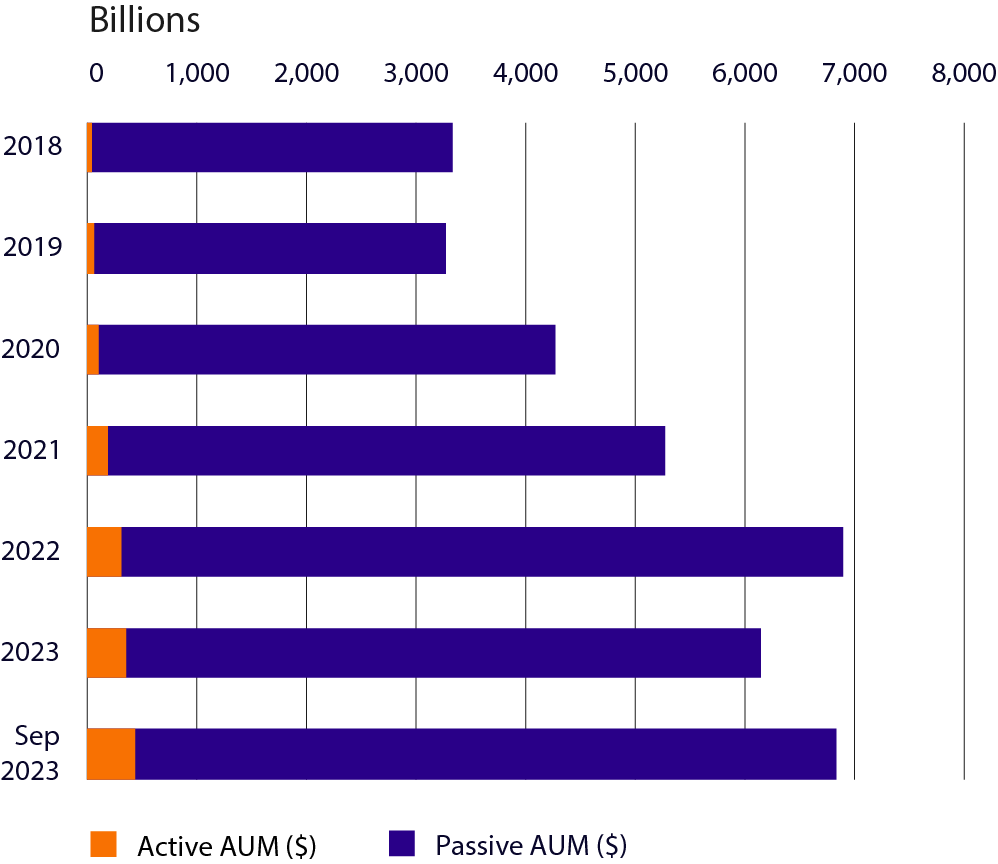

Historically, most exchange traded funds (ETFs) have been passive. But that’s starting to change, with more and more active ETFs coming to market. The growth in active ETFs is largely the result of traditional fund managers realizing that the ETF is a great wrapper and investment vehicle for a broad range of strategies. The result is that investors have more choice than ever before.

Active vs. Passive ETFs Defined

Passive ETFs are designed to track a particular index or sector — and, hence, do not aim to “beat the market.” Rather, they tend to own a basket of securities (based, for example, on market capitalization). The buying, selling and rebalancing process for these strategies is based on a specific set of rules outlined in the product’s methodology.

While they can be rebalanced occasionally if, say, an index is altered, they don’t engage in buying or selling for the purpose of generating excess returns.

Active ETFs, by contrast, are designed with the goal of outperforming a benchmark index or sector. Helmed by professional fund managers, these ETFs may employ a proprietary mix of quantitative and qualitative investment strategies to inform buy and sell decisions. Ideally, an active ETF will deliver ‘alpha’ to investors, that is, a risk-adjusted return that beats a given benchmark.

Why Investors Might Choose Either an Active or Passive ETF

Both styles of ETFs have merits. Passive ETFs might be the right choice for investors who seek index-like returns and prioritizes very low fees. Meanwhile, investors may gravitate toward active ETFs due to a desire to outperform the market — and a belief that their ETF is led by professional managers with the ability to do so.

Source: Nasdaq, as of Oct 23

Differences in Benchmarking: Active vs. Passive ETFs

Active ETFs have more flexibility to choose their reference benchmark or even to choose multiple benchmarks. Active ETF managers can then use the securities and financial instruments within their stated strategy to attempt to outperform their benchmark(s). Conversely, passive ETF managers can choose a specific method to track their one benchmark. Their selection methodology can be full replication, optimization or synthetic replication.

• Full Replication: The ETF holds every security at the same weight as in the benchmark index.

• Optimization: When an index includes more constituents or difficult-to-trade constituents than the ETF can handle in terms of trading costs, the ETF will

hold an optimized sample of the index in terms of costs, correlations and exposure.

• Synthetic Replication: The ETF does not buy the underlying securities of its index and instead uses derivatives to swap the performance of the index for a defined fee. Full disclosure happens on a monthly basis.

Almost all fixed income ETFs use an optimization approach because most fixed income indexes hold thousands of bonds that may or may not have traded recently. The fixed income portfolio manager will utilize a more liquid sample of the bonds to replicate the desired performance.

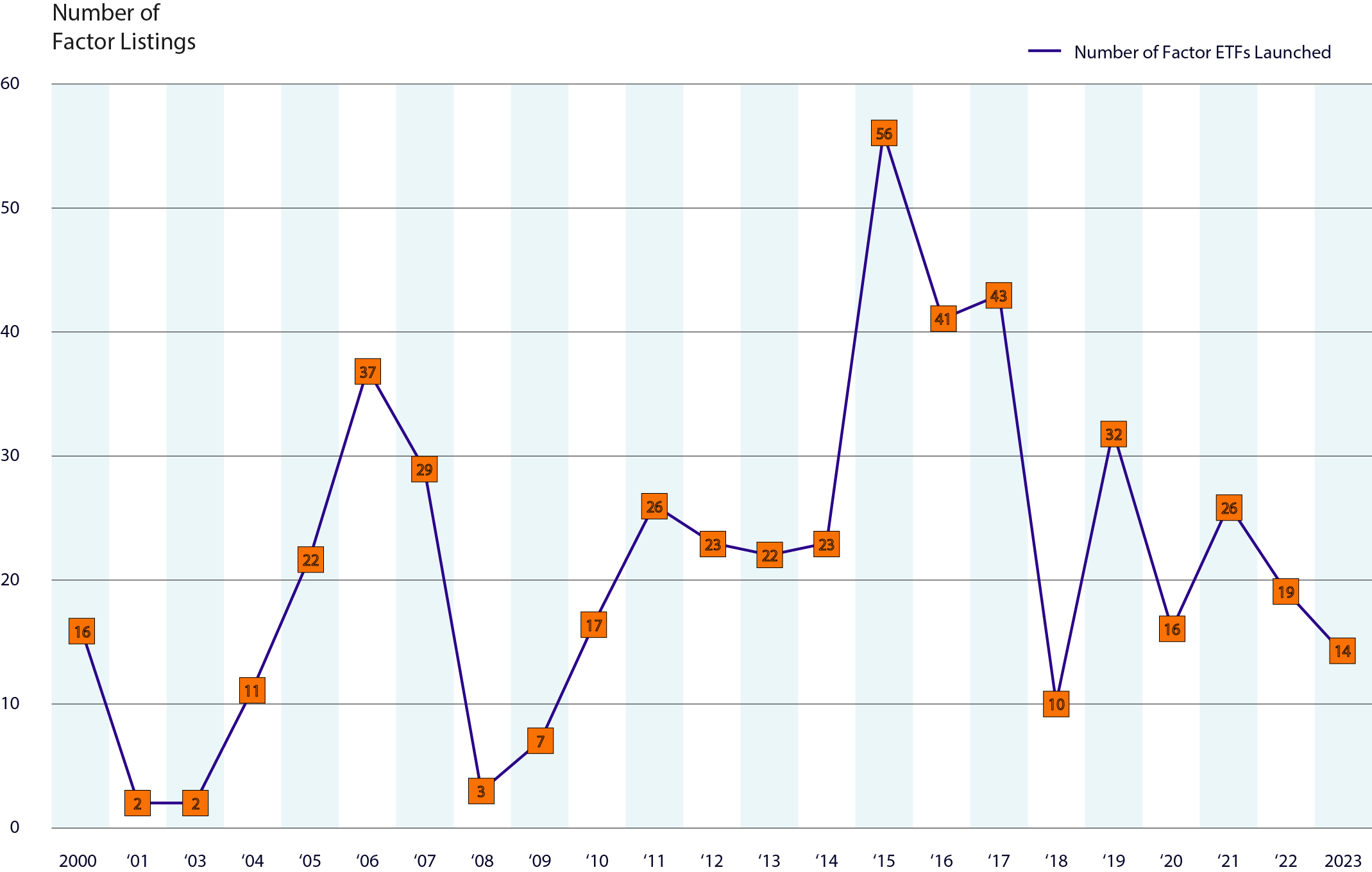

Smart Beta ETFs: A Hybrid Approach to Investment Management

ETFs that combine elements of active and passive approaches employ so called Smart Beta strategies and do not track a straightforward index like the Nasdaq-100® or S&P 500. Rather, these strategies create a more complex set of screening, filtering, weighting and/or rebalancing rules. This could be interpreted as a hybrid approach because it takes the guidelines an active manager may follow and codifies them into a new Smart Beta index that an ETF can track.

Issuers have expanded into launching ETFs focusing on one or more factors that are meant to be used to outperform different parts of the economic cycle as well.

Smart Beta, defined:

Using a rules-based approach instead of discretionary stock-picking.

Source: Nasdaq, as of Oct 23

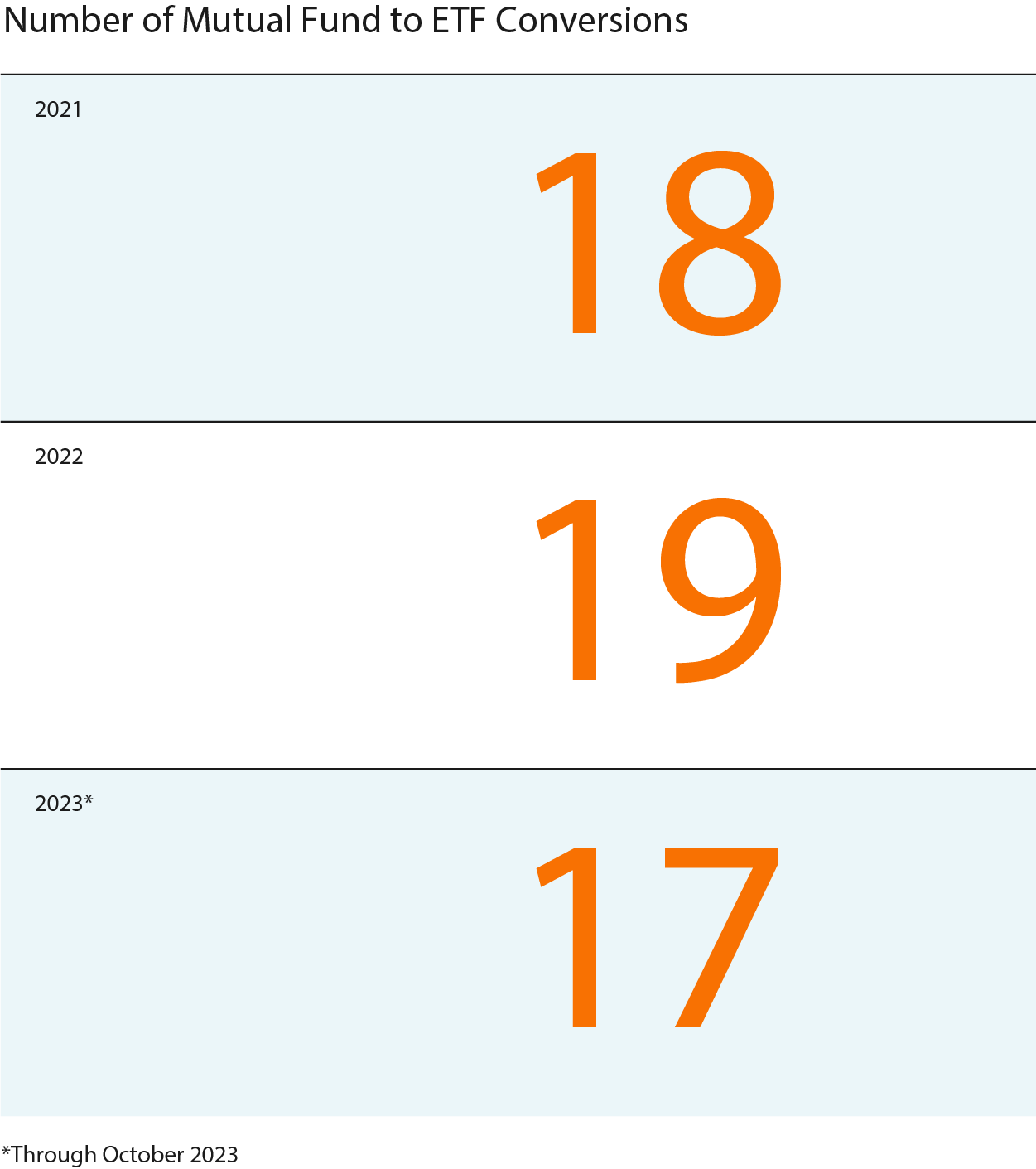

Mutual Fund and Separately Managed Account Conversions to ETFs

The popularity of ETFs among investors shows no signs of abating. As a result, some mutual funds, as well as separately managed accounts (SMAs), are converting to ETFs. Conversions allow for active management offered in a form that can be more tax-efficient, more liquid, more transparent, more accessible (intraday trading/can be purchased on a simple brokerage app) and potentially with lower fees than mutual funds or SMAs. Converting is not without its hurdles, however. The switch from a mutual fund or SMA to an ETF involves operational challenges, significant communication with investors, and in some cases, shareholder approval.

Number of Mutual Fund to ETF Conversions

Source: Nasdaq, as of Oct 23

Conclusion

The scope of ETFs has broadened considerably in recent years. Investors can still access a wide range of passive vehicles, but now have the choice of adding active ETFs to their portfolios. To help ensure you own the ETF that best fits your objectives, understanding the nuances behind the different products is a must.

This resource is brought to you by NASDAQ

Distributed by NASDAQ CAPTIAL MARKETS ADVISORY, LLC, a Registered Broker Dealer and affiliate of Nasdaq, Inc.

Investment Risks

Exchange Traded Products (ETPs) are types of securities that derive their value from a basket of underlying securities such as stocks, bonds, commodities, etc., and trade intra-day on a national securities exchange. Generally, ETPs take the form of Exchange Traded Funds (ETFs) or Exchange Traded Notes (ETNs). Each ETP has a unique risk profile, detailed in its prospectus, offering circular, or similar material, which should be considered carefully when making investment decisions.

Exchange Traded Funds (ETFs) are subject to market risk, including the possible loss of principal. The value of the portfolio will fluctuate with the value of the underlying securities. ETFs may trade at a premium or discount to their net asset value. ETFs may have underlying investment strategy risks similar to investing in commodities, bonds, real estate, international markets or currencies, emerging growth companies, or specific sectors.

Diversification is not a guarantee against loss.

Nasdaq® is a registered trademark of Nasdaq, Inc. The information contained above is provided for informational and educational purposes only, and nothing contained herein should be construed as investment advice, either on behalf of a particular security or an overall investment strategy. Neither Nasdaq, Inc. nor any of its affiliates makes any recommendation to buy or sell any security or any representation about the financial condition of any company. Statements regarding Nasdaq-listed companies or Nasdaq proprietary indexes are not guarantees of future performance. Actual results may differ materially from those expressed or implied. Past performance is not indicative of future results. Investors should undertake their own due diligence and carefully evaluate companies before investing. ADVICE FROM A SECURITIES PROFESSIONAL IS STRONGLY ADVISED.

© 2023. Nasdaq, Inc. All Rights Reserved.