FOMC June 2026 Preview: The Decision Is Settled, the Dot Plot Isn’t

A new Fed Chair, a divided committee, and a decision the market thinks it already knows

On June 17, a new Chair runs his first meeting, the committee is split four ways, and the market has stopped believing the Fed’s own rate path. The decision is near-certain. Everything that matters is in the projections.

Published Tuesday, June 16, 2026 · one day ahead of the June 17 FOMC decision

|

June 17 Decision

HOLD

better than 96% priced (CME FedWatch)

|

2026 Cuts Priced

0

down from ~2 at the start of the year

|

The Gap

1 cut

Fed’s March dots vs. market: none

|

What’s at stake going into Wednesday

On June 17, Kevin Warsh runs his first FOMC meeting as Fed Chair. He was confirmed on May 13 and sworn in as the 17th Chair on May 22, a week after Jerome Powell’s term as Chair ended on May 15. Warsh brings an unusual background to the job: a former Morgan Stanley dealmaker who became the youngest Fed governor ever at 35 and helped manage the 2008 crisis rescues from inside the Board, he holds no economics PhD. The April 28–29 meeting, a third straight hold at 3.50–3.75%, was Powell’s last. Wednesday is the first real read the market gets on how Warsh runs the room.

He inherits a committee that does not agree with itself. April’s hold passed 8 to 4, and the four dissents pulled in opposite directions. Stephen Miran wanted a 25 basis point cut. Beth Hammack, Neel Kashkari, and Lorie Logan backed the hold but objected to the easing bias still sitting in the statement. One dove, three hawks, and an eight-member middle. That is the table Warsh has to manage on day one.

The backdrop makes the job harder. Inflation is running hot, and it just ran hotter. May CPI, released June 10, came in at 4.2% year over year, up from 3.8% in April and the third straight month of accelerating headline inflation. Energy is most of the heat: the conflict with Iran that began in late February and the disruptions around the Strait of Hormuz pushed energy prices up 23.5% over the past year, a jump from 17.9% a month earlier. One reading cut the other way. Core CPI, which strips out food and energy, rose just 0.2% on the month, half of April’s pace, even as its annual rate edged up to 2.9%. The Fed’s preferred gauge, PCE, last ran 3.8% headline and 3.3% core in April; its May update lands only after the meeting. The labor market, meanwhile, refuses to soften: May payrolls came in at +172K against an +80K consensus, revisions added a combined +93K to the prior two months, and unemployment held at 4.3%. Wages are the one clear soft spot, with annual growth easing to 3.4%. For a committee already split on whether to cut, May handed both sides something: a hot headline for the hawks, a cooling core for the doves.

Warsh has signaled he wants to cut anyway. He has called AI “structurally disinflationary” and told the Senate in April that “inflation is a choice.” He has also spent years arguing the Fed fixates on the wrong gauge, dismissing core PCE as “a rough swag” and favoring trimmed-mean measures that have run closer to 2% than to the headline. It is a sharp turn for a man who spent the 2008 crisis warning that inflation was the greater danger. His first set of projections will show whether that instinct survives a string of hot prints and a job market that has not cracked.

That is why this meeting is worth watching even though the decision itself is close to settled. The market prices a hold at better than 96% odds. The signal Wednesday is not the rate. It is the dot plot, the wording of the statement, and the tone of a new Chair in his first press conference.

What the market is pricing

Start with what is already decided. CME FedWatch puts the odds of a hold at the current 3.50–3.75% range above 96%. A cut Wednesday would be a real surprise, and a hike at this meeting is off the table. The suspense sits entirely in the projections that come with the decision.

Where the market has actually moved is the path for the rest of the year. At the start of the year, fed funds futures still pointed to one or two cuts in 2026. That expectation faded as energy prices spiked, and by the March meeting the market’s base case was already no change. The hot inflation prints since have pushed it further still. CME FedWatch, which reads its probabilities off fed funds futures, now puts roughly a four-in-ten chance that the rate sits a quarter-point higher by December, against almost no chance of a cut. The market’s central case is still that the rate holds near today’s 3.6% midpoint through year-end, but the risk it is now pricing is a hike, not a cut.

The Treasury market tells the same story. The five-year yield has climbed about 30 basis points since the March meeting, and the 30-year sits just under 5%. The front end, which tracks the funds rate most closely, has barely moved. That is the shape of a market that has written off near-term cuts and is rebuilding term premium for a Fed that may sit still longer than it once thought. Stocks, for their part, have looked past all of it, with the S&P up about 12% since the March meeting on the same AI-productivity bid Warsh likes to cite.

So the market arrives at Wednesday having already made up its mind: no cuts this year, maybe the opposite. The question is whether the Fed’s own projections still disagree.

The baseline: what the Fed projected in March

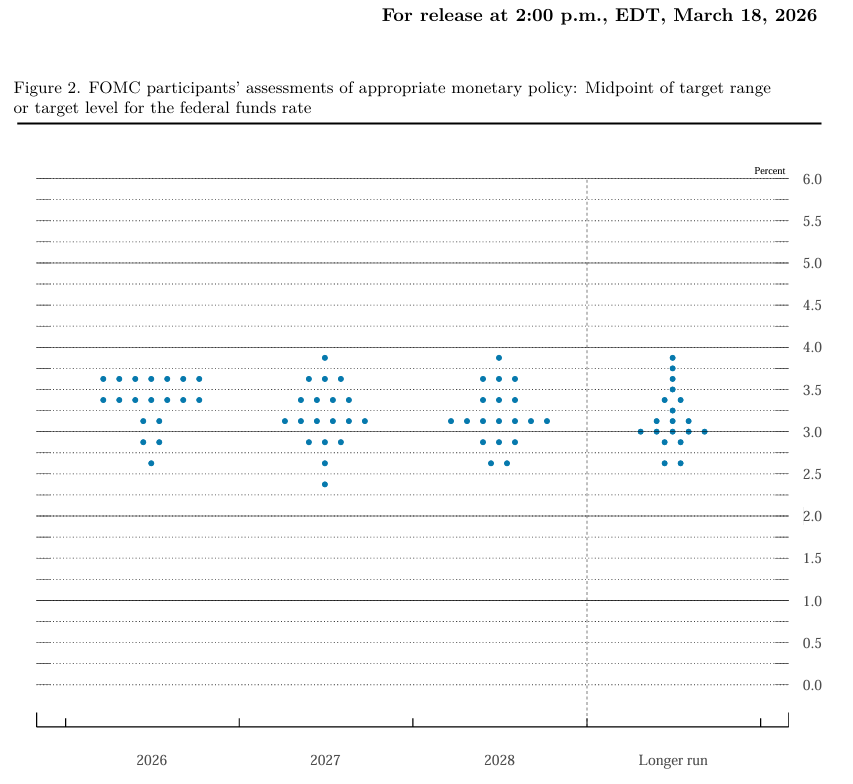

Every quarter the Fed publishes a Summary of Economic Projections, including the “dot plot” (see below) that maps where each official expects rates to go. The June dots only carry meaning against the last set, from the March 18 meeting. Here is that baseline.

Figure 2, FOMC Summary of Economic Projections, March 18, 2026. Each dot is one policymaker’s view of the appropriate year-end fed funds rate (target-range midpoint); the 2026 median sits one cut below today’s rate. Source: Federal Reserve (federalreserve.gov).

In March, the median official saw the federal funds rate ending 2026 at 3.4%, down from the current 3.50–3.75% range. That implied one 25 basis point cut this year, with a second penciled in for 2027. The same projections put 2026 growth at 2.4%, unemployment at 4.4%, and both headline and core PCE inflation at 2.7%.

The inflation figure is the one to hold onto. In March the Fed raised its 2026 PCE forecast to 2.7%, up from the 2.4% it projected back in December. It saw inflation finishing the year well above its 2% target and still kept a cut in the outlook. The committee judged that cut appropriate even with oil prices climbing. The longer-run rate held at 3.1%, so the Fed’s view of where rates settle over time did not budge.

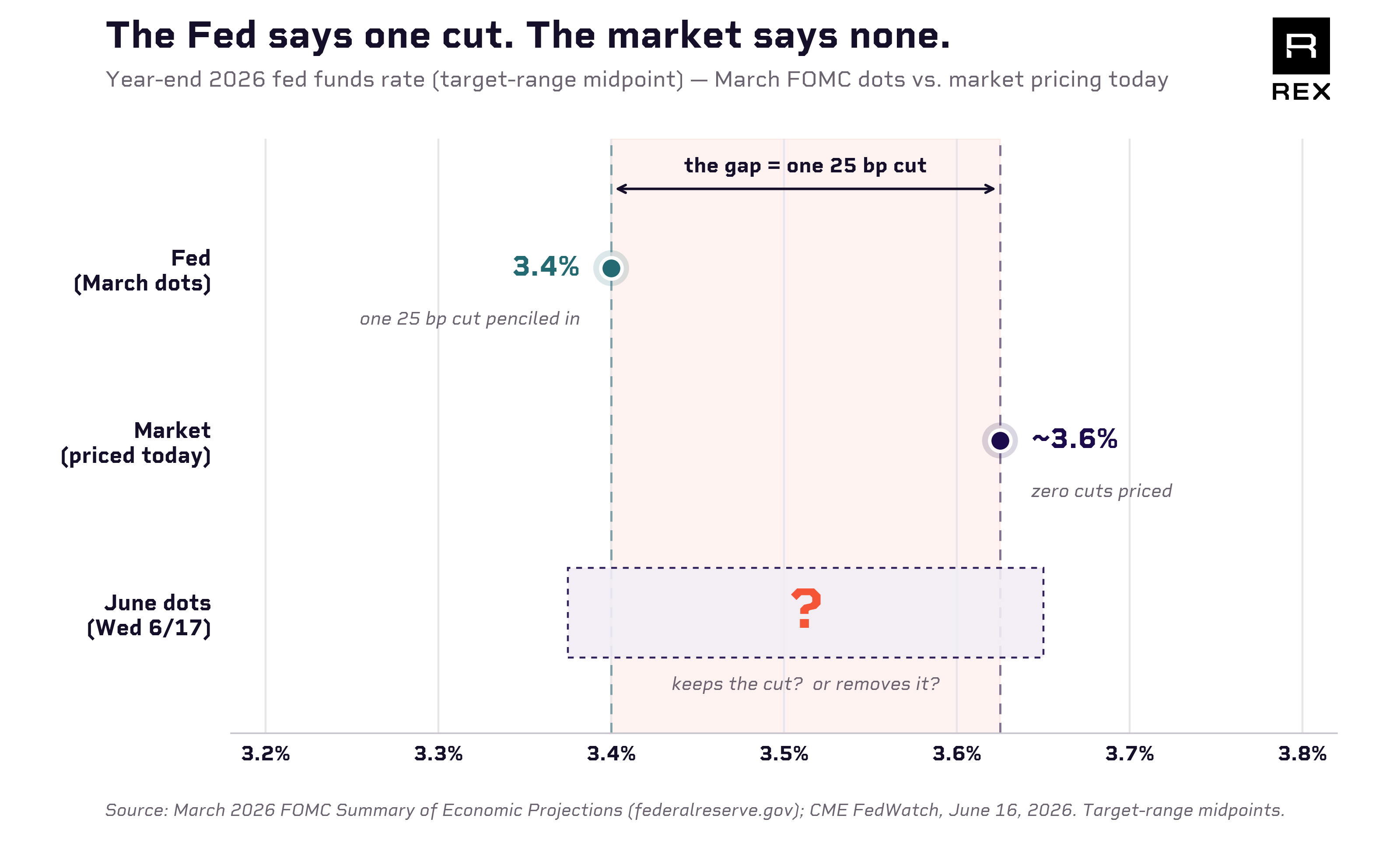

Put that March projection next to where the market sits today and the daylight is easy to see. The committee’s last word was one cut in 2026. The market’s current word is none, with a lean toward a hike. That is the gap Wednesday’s dot plot begins to settle.

Year-end 2026 fed funds rate (target-range midpoint): the Fed’s March dots vs. market pricing today. The gap is one 25 bp cut. Source: March 2026 FOMC Summary of Economic Projections (federalreserve.gov); CME FedWatch.

If the June median still shows one 2026 cut, Warsh’s committee is holding its dovish lean against the inflation data and moving toward the market only on paper. If the cut drops out and the year-end median climbs to 3.6% or higher, the Fed is confirming what the market already believes. The March baseline above is the number the new projection gets measured against.

What to watch Wednesday

The statement and the new projections land at 2:00 p.m. ET, and Warsh takes questions half an hour later. Four things will tell you how his first meeting went.

- The dot plot. The single most important number is the 2026 median. In March it sat at 3.4%, one cut below today’s rate. If it holds there, Warsh is defending a dovish lean against three straight months of hot inflation. If the cut drops out and the median moves to 3.6% or higher, the Fed is conceding the point the market has already priced. A median that adds a hike would be the genuine shock. Warsh has also suggested the dot plot should become “a relic.” The projection the whole market is about to parse may be among the last of its kind.

- The dissents. April’s hold passed 8 to 4, with one official wanting a cut and three objecting that the statement read too dovish. Managing that split is Warsh’s first real test. Watch the tally and the names. Fewer dissents would say he pulled the committee toward consensus; more, or a louder hawkish bloc, would say the divide is widening as inflation runs hot.

- The statement redline. April’s language still leaned toward eventual easing and pinned elevated inflation partly on energy. Whether that easing bias survives, and how the committee now describes inflation, is the cleanest read on where the center of the room sits.

- Warsh himself. This is the first time the market hears Warsh run a press conference as Chair. He built his case on the idea that AI is structurally disinflationary and that the Fed can afford to look through some of the current heat, and May’s cooling core hands him a data point to do exactly that even with the headline at 4.2%. His tone, and whether he sounds like a Chair preparing to cut or one boxed in by the data, will move markets as much as the dots.

The rate is settled. Everything that matters Wednesday is in how a new Chair frames a call the market thinks it has already made.

Sources: Federal Reserve March 2026 Summary of Economic Projections and April 2026 FOMC statement (federalreserve.gov); U.S. Bureau of Labor Statistics Consumer Price Index (May 2026, released June 10) and Employment Situation (May 2026); CME FedWatch, derived from 30-Day Fed Funds futures, as of June 2026; Treasury yields and equity levels from daily closing data since the March 18, 2026 FOMC. Kevin Warsh public statements: Senate Banking Committee testimony (April 21, 2026) and Hoover Institution lectures. This is editorial market commentary, not investment advice. All figures in U.S. dollars and as of mid-June 2026.