REX Autocallable Income ETF (ATCL) April 2026 Commentary

April Recap: Half the Market’s Volatility, Coupons Intact

Key Highlights

- April Distribution: 1.13%

- Distribution Rate: 13.60%

- 30-Day SEC Yield: 2.71%

- April Performance: ATCL: 5.26% | SPXT: 10.49%

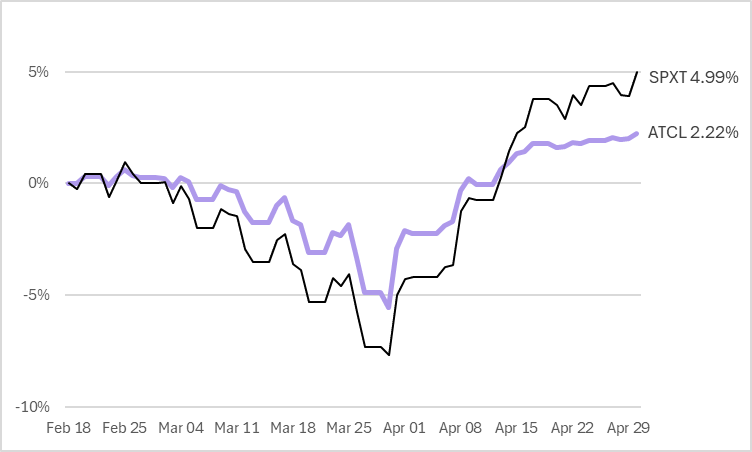

- Since Inception Performance (2/18 – 4/30/26): ATCL: 2.22% | SPXT: 4.99%

- Since Inception Beta to S&P 500 TR: ~0.7

- Since Inception Upside Capture: ~60% of S&P 500 TR Index

- Since Inception Downside Capture: ~65% of S&P 500 TR Index

The 30-Day Yield represents net investment income earned by the Fund over the 30-Day period ended 4/30/2026, expressed as an annual percentage rate based on the Fund’s share price at the end of the 30-Day period. The 30-Day unsubsidized SEC Yield does not reflect any fee waivers/reimbursements/limits in effect.

The Distribution Rate is the annual rate an investor would receive if the most recently declared distribution, which includes option income, remained the same going forward. The Distribution Rate is calculated by multiplying an ETF’s Distribution per Share by twelve (12), and dividing the resulting amount by the ETF’s most recent NAV. The Distribution Rate represents a single distribution from the ETF and does not represent its total return. The distribution may include a combination of ordinary dividends, capital gain, and return of investor capital and has the potential to change during any given tax year. Please refer to the 19a-1 Notice, which can be located on the Fund’s website, regarding the composition of distributions, including return of capital. Final determination of a distribution’s tax character will be made on Form 1099 DIV.

Beta measures the sensitivity of a fund’s returns relative to a benchmark index.

Upside Capture measures how much of a benchmark’s positive returns a fund participates in during periods when the benchmark rises.

Downside Capture measures how much of a benchmark’s negative returns a fund participates in during periods when the benchmark declines.

Commentary

- Structured product issuance remained elevated in April, with equity-linked issuance totaling $18B, up 25% year-over-year.

- Equity markets rallied sharply in April, with the S&P 500 TR Index returning 10.49%, as the April 8 US-Iran ceasefire agreement triggered a broad relief rally. Markets appear to be pricing in an eventual normalization of Strait of Hormuz shipping traffic.

- ATCL returned +5.26% in April, delivering strong absolute performance with annualized volatility of just 6.01% — roughly half that of the S&P 500 TR Index (11.72%). The portfolio’s weighted average mark-to-market level rose to 96% from 93% in March, supported by the rally in equity markets. Coupon accrual across the portfolio continues to contribute to total returns.

- Portfolio positioning remains constructive, with all positions currently above their coupon barriers, supporting full coupon eligibility across the portfolio.

- ATCL paid its second distribution in April, with an annualized distribution rate of 13.60%, of which 87.1% was estimated as Return of Capital.

The coupon is the annualized percentage of the notional amount allocated to an Autocallable Contract at the Observation Dates.

The performance data quoted represents past performance and is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent Standardized Performance and month-end performance, please call 1-844-802-4004.

Portfolio Highlights

| Live Autocallables | 287 |

| Weighted Avg. Coupon | 14.26% |

| Weighted Avg. MTM Discount | 96.42% |

| % Above Coupon Barrier | 100% |

| Autocallables with Principal at Risk | 0 |

Live Autocallables: shows how many autocallables are still outstanding and have not yet been called or matured.

Weighted Avg. Coupon: Shows the weighted average yearly coupon currently paid across all active autocallables. Distribution percentage shown is preliminary. The final distribution amount will be set by the fund manager.

Weighted Avg. MTM Discount: Shows the average current market price of live autocallables as a percentage of par (100%), weighted by position size.

Autocallables with Principal at Risk: Shows number of autocallables currently below maturity barriers and with one year or less until maturity.

Performance Summary

April: 4/1 – 4/30/26 • Since Inception: 2/18 – 4/30/26 (ATCL inception: 2/18/26)

| Ticker | Fund Name | April | Since Inception |

|---|---|---|---|

| ATCL | REX Autocallable Income ETF (NAV) | 5.26% | 2.22% |

| SPXT | S&P 500 Total Return Index | 10.49% | 4.99% |

For current standardized performance, click here.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Performance current to the most recent month-end can be obtained by calling 1-844-802-4004.

The Fund’s gross expense ratio is 0.74%.

Since Inception Cumulative Return

Data as of 4/30/26. Source: Bloomberg. Daily total returns. Inception: February 18, 2026. Past performance is not indicative of future results.

The Fund enters into swap agreements with RBC to obtain exposure to the Bloomberg US Large Cap VolMax Autocallable Total Return Index. RBC is not an advisor, promoter, in any way affiliated with the Fund and has no responsibility for the Fund’s performance, marketing, or trading, or any responsibility regarding the suitability of the Fund as an investment.

Investing in the Fund involves a high degree of risk. As with any investment, there is a risk that you could lose all or a portion of your investment in the Fund.

This information must be preceded or accompanied by a prospectus. Before investing you should carefully consider the Fund’s investment objectives, risks, charges and expenses. This and other information is in the prospectus. Please read the prospectuses carefully before you invest. Investments involve risk. Principal loss is possible. For ATCL prospectus, click here.

THE FUND, TRUST, AND ADVISER ARE NOT AFFILIATED WITH THE BLOOMBERG US LARGE CAP VOLMAX AUTOCALLABLE TOTAL RETURN INDEX, THE BLOOMBERG US LARGE CAP VOLMAX INDEX, THE BLOOMBERG US LARGE CAP TOTAL RETURN INDEX, OR BLOOMBERG LP.

Autocallable Structure Risk. The Fund’s returns are linked to a structured autocallable index, which may limit upside participation and expose investors to complex payoff patterns that differ from direct investments in the underlying securities.

Barrier Risk. If the underlying reference index breaches specified barrier levels, principal and income protections may be reduced or lost, potentially resulting in significant losses of invested capital.

Coupon/Contingent Income Risk. Coupon payments are contingent on barrier conditions being met and are not guaranteed; in unfavorable market environments, investors may receive little or no income.

Early Redemption Risk. Autocallable features can cause positions to be redeemed early in rising markets, forcing reinvestment at potentially lower yields and limiting participation in continued market gains.

Market Risk. The value of the Fund will fluctuate with overall market conditions and the performance of the underlying reference index, and investors could lose money, including principal.

Volatility Target Index Risk. The volatility-targeted reference index may underperform traditional equity indices because of its leverage caps, volatility adjustment mechanism, and embedded financing or cost overlays.

Active Management Risk. The Fund’s performance depends on the investment decisions and risk management techniques of the adviser, which may not achieve the intended results and could cause the Fund to underperform.

Liquidity Risk. Certain instruments, including derivatives referencing structured notes or indices, may become difficult or costly to trade, which can impact pricing, portfolio management, and the ability to meet redemptions.

Derivatives Risk. The Fund’s use of derivatives may magnify gains and losses, introduce leverage, and create exposure to valuation, correlation, and operational risks that can adversely affect performance.

Options Contracts Risk. Options can expire worthless, are sensitive to changes in volatility, time decay, and the price of the underlying asset, and may be less liquid than other securities.

New Fund Risk. Because the Fund is newly formed, it has a limited operating history and there can be no assurance that it will be successful in implementing its investment strategy.

Underlying Reference Index and Volatility Targeting Risk. Performance depends on the Bloomberg US Large Cap VolMax Index (or any successor index), which applies volatility targeting, financing charges and other adjustments that may cause it to underperform the underlying equity index.

Equity Market Risk. The value of the Fund may fluctuate in response to stock market moves, and equity markets can decline rapidly and unpredictably.

Debt Securities and U.S. Treasury Risk. Investments in U.S. Treasuries and other debt used as collateral are subject to interest-rate, credit, prepayment and liquidity risk, which can negatively impact the Fund.

Non-Diversification Risk. As a non-diversified fund, the Fund may invest a larger portion of its assets in fewer issuers or strategies, increasing the impact of any single position or market event on performance.

Concentration Risk. To the extent the Fund concentrates its investments in specific sectors, asset classes, or strategies, it is more vulnerable to conditions and events that adversely affect those areas.

Counterparty Risk. The Fund is exposed to the creditworthiness of swap, options, and other transaction counterparties, and could incur losses if a counterparty fails to meet its obligations.

Cyber Security Risk. The Fund and its service providers may be adversely affected by cyber-attacks or other information security events that could result in financial loss, business disruption, or unauthorized access to confidential information.

Funds distributed by: Foreside Fund Services, LLC, not affiliated with Rex Shares, LLC, or its affiliates.