NVIDIA Q1 FY27 Earnings: Reading the AI Capex Curve

NVIDIA Q1 FY27: Reading the AI Capex Curve

The four largest hyperscalers spent $130.6B on capex in Q1 2026, up +193% in nine quarters. A meaningful share of it cycles through one P&L. The Q1 print and Q2 FY27 outlook are below.

Published Wednesday, May 20, 2026 · Updated 5:00pm ET with the print and Q2 FY27 outlook

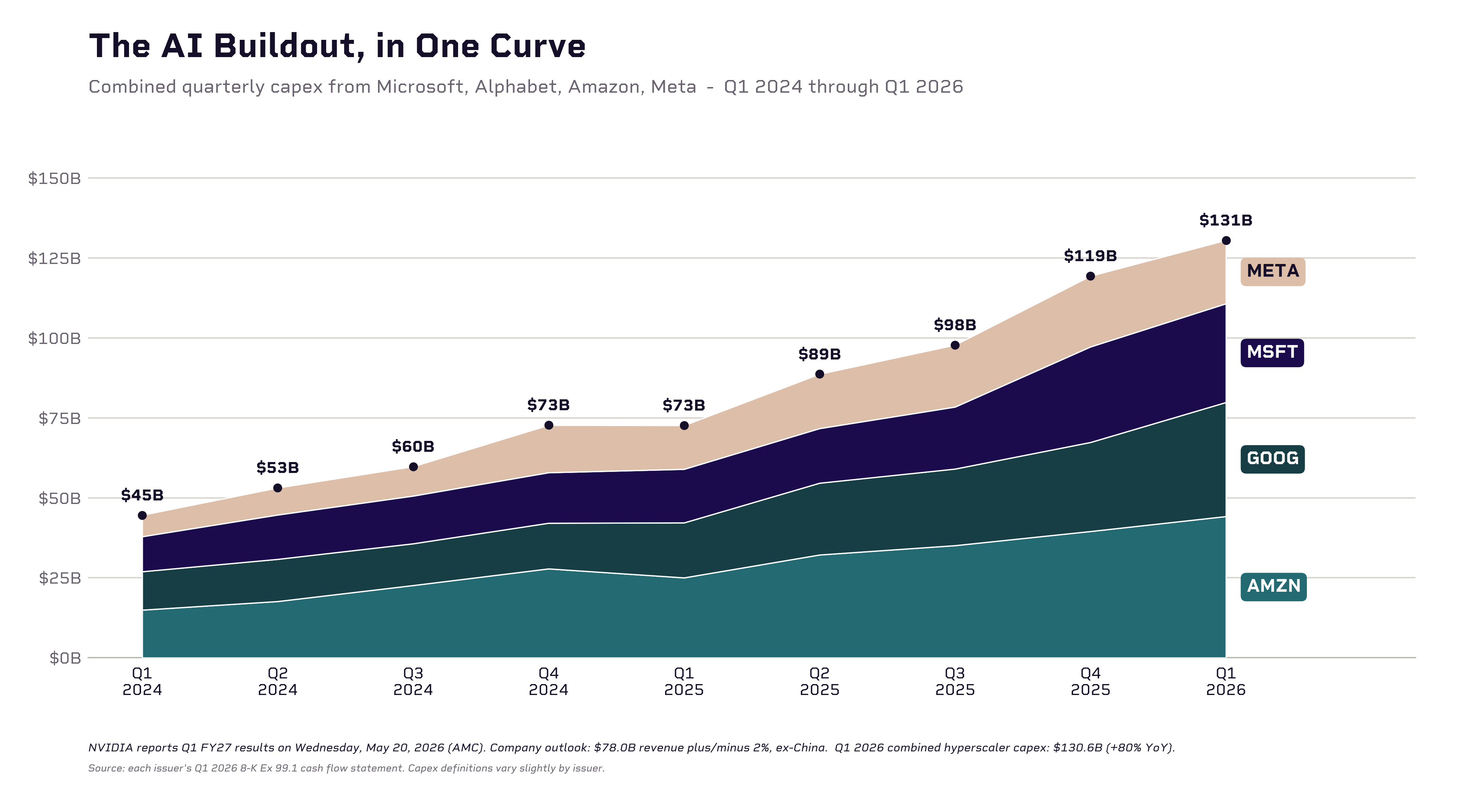

Hyperscaler capex, stacked by company. Q1 2024: $44.6B → Q1 2026: $130.6B (+193%). Source: each issuer’s Q1 2026 8-K Ex 99.1 / cash flow statement.

|

Q1 2026 Hyperscaler Capex

$130.6B

+193% over 9 quarters

|

MSFT RPO + GOOG Cloud Backlog

$1T+

MSFT +99% YoY · GOOG ~doubled QoQ

|

Consensus-Implied Beat

+1.0%

Smallest in 12-quarter streak

|

The Setup

- Q1 FY27 consensus revenue: $78.79B (+79% YoY vs. $44.06B in Q1 FY26)

- Q1 FY27 consensus EPS: $1.77 (+119% YoY vs. $0.81 in Q1 FY26)

- Company guide (issued Feb 25, 2026): $78.0B ± 2% ($76.4B–$79.6B), explicitly excluding any Data Center compute revenue from China

- Q4 FY26 baseline: $68.1B revenue, $62.3B Data Center (91.4% of mix), 75.0% GAAP gross margin, $1.76 GAAP EPS

Consensus figures pulled May 12, 2026. Guide figures from NVIDIA’s Q4 FY26 outlook statement (8-K, accession 0001045810-26-000019, filed Feb 25, 2026).

Pre-Print Commentary

- The customers already told you the quarter. The four largest hyperscalers (Microsoft, Alphabet, Amazon, and Meta) together spent $130.6B on capital expenditures in Q1 2026. That is up +80% year-over-year and +193% over the nine quarters since Q1 2024. NVIDIA’s Q1 FY27 guide of $78.0B is the supplier-side echo of that spend. The lead time between hyperscaler capex commitments and NVIDIA revenue has historically been one to two quarters.

- Backlog you can see. Microsoft’s Commercial Remaining Performance Obligations, the contracted-but-not-yet-recognized revenue under signed enterprise cloud deals, doubled year-over-year to $627B in Q1 2026 (+99% YoY). Alphabet disclosed Google Cloud backlog above $460B, roughly doubled quarter-over-quarter. More than $1 trillion of contracted future cloud revenue sits behind the order book of NVIDIA’s largest customers.

- The China bracket. Q1 FY26 included a $4.5B H20-related charge that depressed the year-ago base. NVIDIA’s Q1 FY27 guide explicitly excludes any Data Center revenue from China. The +79% YoY consensus reflects both real growth and a clean base comp.

- What guidance does to the curve. The Q1 print itself is partially known. The Q2 FY27 outlook is where the story diverges. A guide above the consensus run-rate would signal hyperscaler capex still has room to compound; a guide below would mark the first inflection in the AI infrastructure cycle.

Hyperscaler Cross-Read

The four largest buyers of accelerated compute reported Q1 2026 the last week of April. Their capex and backlog disclosures are NVIDIA’s leading indicator. The lead time between hyperscaler commitments and NVIDIA revenue is one to two quarters.

| Company | Q1 2026 Capex | Y/Y | Forward Signal |

|---|---|---|---|

| Microsoft (MSFT) | $30.9B | +84% | Commercial RPO $627B (+99% YoY) |

| Alphabet (GOOG) | $35.7B | +107% | Cloud backlog $460B+, roughly doubled QoQ |

| Amazon (AMZN) | $44.2B | +77% | “Fastest AWS growth in 15 quarters” |

| Meta (META) | $19.8B | +45% | FY26 capex guide raised to $125–145B from $115–135B |

| Combined | $130.6B | +80% | NVDA Q1 FY27 guide: $78.0B |

Capex commitments do not flow one-for-one into NVIDIA revenue. Hyperscalers spend on real estate, power, networking, and CPU servers alongside GPUs. But the directional signal is hard to miss: when the four largest buyers of accelerated compute collectively spend $130B in a single quarter, the company that supplies the silicon does not get to print a small number.

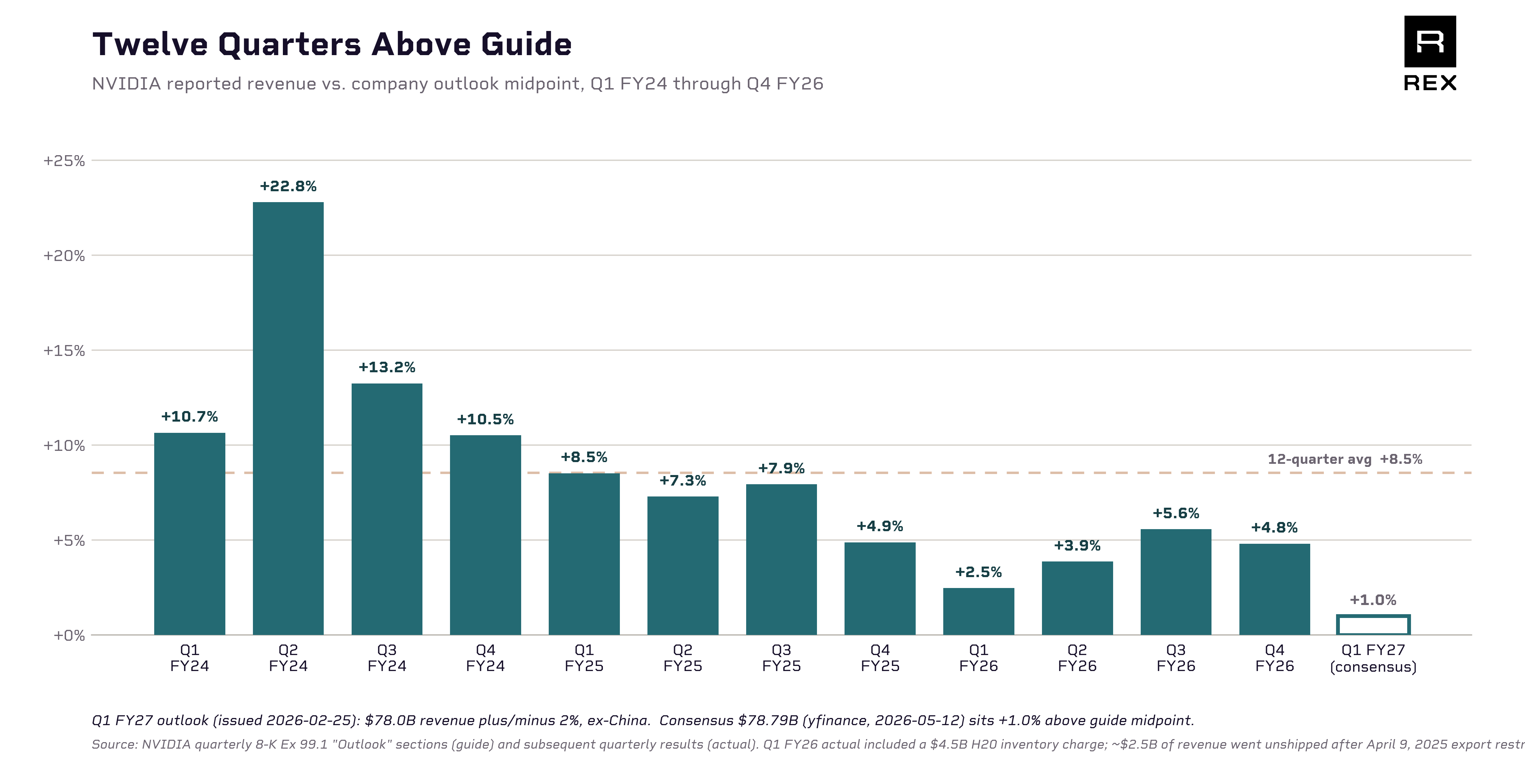

Twelve Quarters of Beating Their Own Guide

NVIDIA quarterly revenue: guide midpoint vs. reported. 12 straight quarters above guide, with beat magnitude compressing from +22.8% (Q2 FY24) toward the +1.0% consensus implies for tonight. Source: NVIDIA earnings releases (8-K filings).

|

FY24 · Hopper

+14.3%

avg beat

|

FY25 · Blackwell ramp

+7.2%

avg beat

|

FY26 · Steady-state

+4.2%

avg beat

|

Q1 FY27 · Tonight

+1.0%

consensus implied

|

Twelve straight beats, but the magnitude is compressing toward the guide. Whether tonight’s print holds the streak, and at what magnitude, is the first thing to read off the wire. The second is whether the Q2 FY27 outlook continues to track the hyperscaler capex curve, or starts to lag it.

What to Watch Tonight

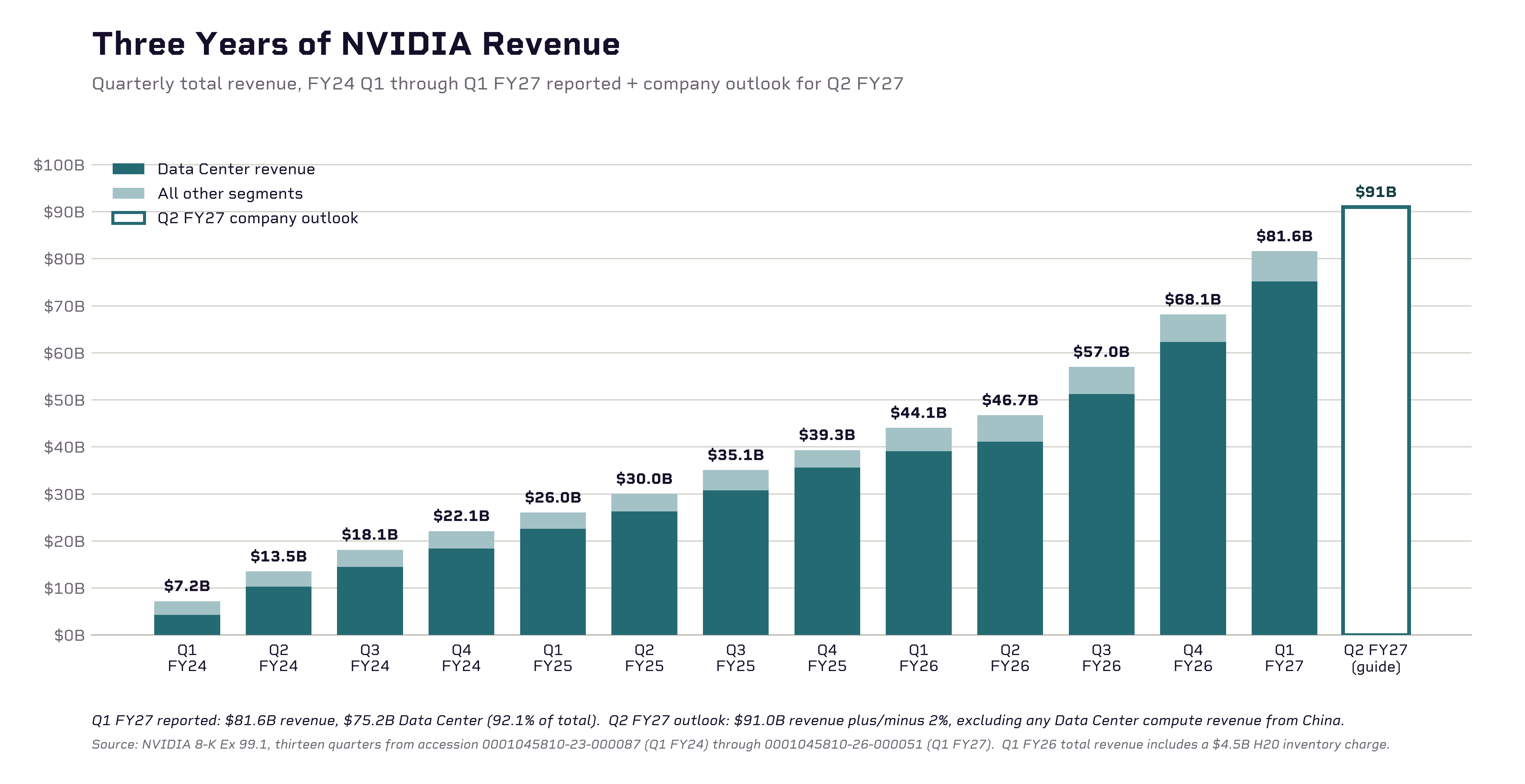

- Data Center segment revenue. Q4 FY26 printed at 91.4% of total. Anything north of $70B in Data Center confirms the trajectory; a print materially below that, on otherwise in-line total revenue, would signal mix is shifting.

- Q2 FY27 guide. The print itself is largely written by Q1 capex from MSFT, GOOG, AMZN, META. The forward guide is the company’s read on whether that capex curve compounds.

- Gross margin trajectory. GAAP gross margin recovered from the Blackwell-ramp trough back to 75.0% in Q4 FY26. Q1 FY27 guide: 74.9%. Any pressure here is the bear case’s only real handhold.

- China commentary. The Q1 FY27 guide explicitly excludes China Data Center compute. Any color on H20, export-control developments, or sovereign-AI workarounds would reshape the FY27 base.

- Capital return. $58.5B remained on the buyback authorization at Q4. FY26 returned $41.1B in total ($40.1B buybacks + $1.0B dividends). Any new authorization is a tell on management’s read of the runway.

The Print

Updated 5:00pm ET, May 20, 2026

|

Revenue

$81.6B

vs. $78.79B est. · +85% YoY

|

Non-GAAP EPS

$1.87

vs. $1.77 est. · +140% YoY

|

Data Center

$75.2B

92.1% of total · +92% YoY

|

- Beat streak: held at 13 quarters. Revenue beat the guide midpoint by +4.6% ($81.6B vs. $78.0B), slightly above the FY26 average beat of +4.2% and well above the +1.0% the consensus had implied.

- Gross margin: GAAP 74.9% (in line with the 74.9% guide); Non-GAAP 75.0%. No re-acceleration, no compression. The Blackwell-ramp margin profile is holding at steady-state.

- Q2 FY27 guide: $91.0B ± 2%, explicitly excluding any Data Center compute revenue from China. That is +11.5% sequential and +94.7% year-over-year at the midpoint, accelerating from the +85.2% YoY just printed.

- Data Center sub-segments: Compute $60.4B (+77% YoY, +18% QoQ); Networking $14.8B (+199% YoY, +35% QoQ). Networking continues to scale faster than compute.

- Capital return: Board approved an additional $80.0B share repurchase authorization on May 18 and raised the quarterly cash dividend from $0.01 to $0.25 per share. $38.5B remained on the prior authorization at quarter-end; ~$20B was returned to shareholders during Q1.

- Reporting framework change: Starting next quarter NVIDIA will report two market platforms: Data Center (split into Hyperscale and ACIE for AI Clouds, Industrial and Enterprise) and Edge Computing.

NVIDIA quarterly total revenue, Q1 FY24 through Q1 FY27 reported, plus the Q2 FY27 company outlook ($91.0B). Data Center segment shown in solid teal. Source: NVIDIA 8-K Ex 99.1, accession 0001045810-26-000051.

What It Tells Us

The customers’ signal flowed through. $130.6B in collective Q1 hyperscaler capex showed up as a $75.2B Data Center quarter on the supplier side. The lead time held. The beat vs. guide midpoint was +4.6%, slightly above the FY26 steady-state pace and three-plus turns above the +1.0% the sell-side had centered on. The compression narrative in the multi-year beat chart was real, but the FY27 starting point lands a step above the FY26 cadence rather than below it.

The forward guide is where the picture changes. $91.0B for Q2 FY27 implies +94.7% year-over-year growth at the midpoint, an acceleration from the +85.2% just printed. That is unusual at this scale; year-over-year growth on a base this large normally compresses, not expands. The guide assumes zero Data Center compute revenue from China. Two readings: either hyperscaler Q2 capex commitments are pulling forward faster than the Q1 capex print suggested, or NVIDIA is taking a larger share of total accelerated-compute spend than the customer-side disclosures alone capture. The supplier-side data point now leads the customer-side filings, not the other way around.

The capital return is the second-order signal. An incremental $80.0B buyback authorization on top of the $38.5B remaining is roughly $118.5B of available repurchase capacity. The dividend raise from $0.01 to $0.25 per quarter is the more readable disclosure: a recurring distribution commits forward cash flow in a way authorizations do not. Both are management’s read of runway, expressed in dollars rather than language.

What didn’t move: gross margin. GAAP 74.9% printed exactly at guide; Non-GAAP 75.0% landed within 10bps of Q4’s 75.1%. The Blackwell-ramp pressure that compressed margin earlier in FY25 has not returned. Gross margin was the one item flagged in the pre-print “What to Watch” list that could have reframed the quarter, and it landed on the line.

Sources: NVIDIA Q1 FY27 8-K (accession 0001045810-26-000051, filed 2026-05-20); NVIDIA Q4 FY26 8-K (accession 0001045810-26-000019, filed 2026-02-25); Microsoft Q3 FY26 8-K (filed 2026-04-29); Alphabet Q1 2026 8-K (filed 2026-04-29); Amazon Q1 2026 8-K (filed 2026-04-29); Meta Q1 2026 8-K (filed 2026-04-29). Consensus estimates pulled from yfinance on 2026-05-12. Capex figures sourced from each company’s quarterly cash flow statement. All figures presented in U.S. dollars.