How Leveraged ETFs Work: The Math of Daily Rebalancing

How Leveraged ETFs Work: The Math of Daily Rebalancing

Why does a 2× ETF lose money even when the underlying ends the year flat? The answer comes down to the math of compounding daily returns. Once you see it, the design of every leveraged ETF starts making sense.

The Daily Reset Is Doing Exactly What It Says

A 2× daily leveraged ETF has one job: deliver 2× the underlying’s return on any single trading day. If the underlying goes up 1% today, the ETF aims to go up 2%. If the underlying drops 1%, the ETF drops 2%. That’s the daily objective, and every business day, the fund delivers on it.

To keep that promise, the fund rebalances every day. At each market close, the fund’s exposure is reset so that the next day starts at exactly 2× the new NAV. This is the mechanical part most investors don’t picture: a 2× ETF resets its leverage every single trading session.

The rebalancing logic is mechanically simple: when the underlying rises, the fund increases its exposure (it needs more notional to maintain 2× on a now-larger NAV). When the underlying falls, the fund decreases its exposure (less notional needed to maintain 2× on a now-smaller NAV).

That pattern (adding exposure after gains, cutting it after losses) is structurally the same as buying high and selling low. In a market that trends one direction, that pattern actually helps (more on this in a moment). In a market that chops sideways, it hurts. The math is the same in both cases; only the path changes.

Why “2× Daily” Is Not “2× Over Any Other Period”

Here is the cleanest possible illustration. Imagine an underlying stock priced at $100. Over two trading days, it moves up 10%, then back down 9.09%, ending exactly where it started. Now what happens to a 2× ETF tracking it?

| Day | Underlying Move | Underlying Price | 2X ETF Move | 2X ETF Price |

|---|---|---|---|---|

| Start | $100.00 | $100.00 | ||

| End of Day 1 | +10.00% | $110.00 | +20.00% | $120.00 |

| End of Day 2 | −9.09% | $100.00 | −18.18% | $98.18 |

The underlying ended exactly where it started. The 2× ETF ended down 1.82%. Two days, no fees, no tracking error. Just the math of compounded daily returns.

The reason is asymmetric base sizes. The 10% gain and the 9.09% loss are equal in price terms. They each represent a $10 move that cancels out at the underlying level. But for the 2× ETF, the +20% on Day 1 is applied to a $100 base ($20 gain), while the −18.18% on Day 2 is applied to a $120 base ($21.82 loss). The percentage moves are still 2× the underlying’s, but they’re being applied to different dollar amounts. That asymmetry compounds.

Stretch this across 252 trading days of a volatile but sideways underlying, and the asymmetry stops being a rounding error and becomes the dominant feature of the return.

Volatility Decay: The Bigger the Swings, the Bigger the Gap

The two-day example shows the math working over two days. Picture the same math over a full year.

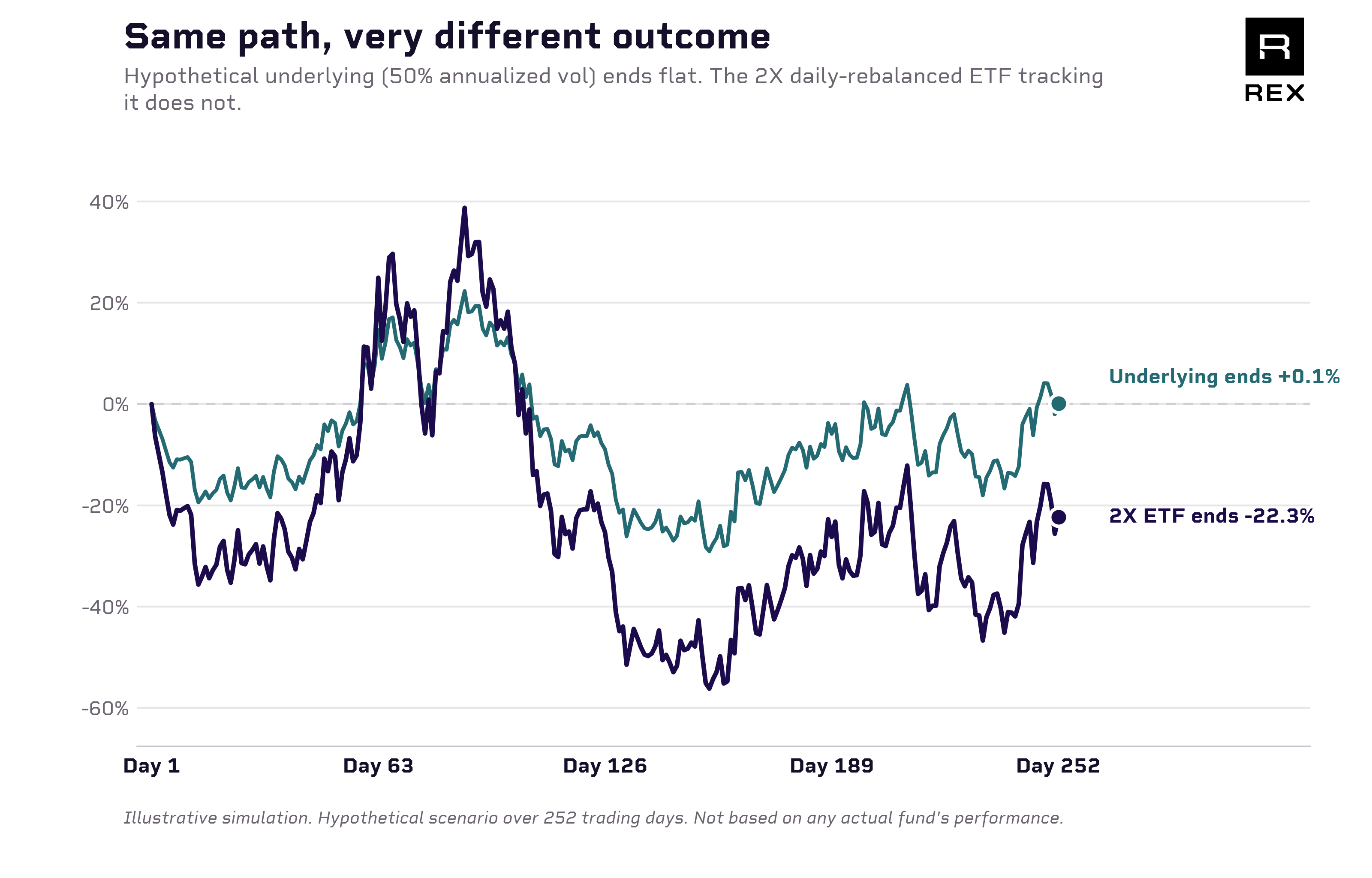

In the chart at the top of this post, both lines start at zero. They move with the same daily ups and downs; the 2× ETF just doubles each day’s move in the underlying. Over a year of trading, the underlying bounces around and ends roughly flat. The 2× ETF, riding the same path at double size, ends the year down about 22%.

How big that gap is depends on how choppy the year was. The more the underlying moved around day-to-day (its volatility), the bigger the gap. And the relationship grows fast: when volatility doubles, the gap more than triples.

|

30% Vol

−9%

expected 1-yr decay

|

50% Vol

−22%

expected 1-yr decay

|

70% Vol

−39%

expected 1-yr decay

|

100% Vol

−63%

expected 1-yr decay

|

A calm, blue-chip-style stock might cost a 2× holder around 9% over a flat-but-bumpy year. A volatile single-stock name riding 70-100% daily-swing volatility can cost 40-60% or more over the same flat year. Same starting price. Same ending price. Very different outcomes inside a 2× ETF.

That’s how compounding works when daily moves get doubled. The product is doing exactly what its prospectus says. The mismatch is between how “2× leveraged” sounds like it should behave, and what daily rebalancing math actually produces.

The Other Side of the Coin: When 2× Can Outperform 2×

A complete picture of the math has to include the cases where compounding works for the holder, not against. The “buying high, selling low” rebalancing pattern only erodes returns when the market chops sideways. In a market that trends consistently in one direction, the same daily rebalancing actually amplifies the cumulative return beyond a simple 2× multiplier.

The mechanism is straightforward. In a strong uptrend, the fund’s exposure keeps growing each day; it’s adding to a position that keeps winning. After many consecutive up-days, the cumulative return can exceed 2× the underlying’s cumulative return, sometimes by a wide margin. The same effect runs in reverse for a strong downtrend: in a sustained selloff, an inverse or downside-leveraged fund can outperform its multiple as exposure compounds in the direction of the move.

Here’s how the same math plays out across different market regimes:

- Trending markets: Daily compounding boosts returns relative to a simple multiple.

- Choppy, range-bound markets: Daily compounding erodes returns.

- Low-volatility markets: The compounding effect (in either direction) is small.

- High-volatility markets: The compounding effect is large, in whichever direction the path determines.

What this means for holders is that the return of a leveraged ETF over any period longer than one day depends on the path, not just the endpoints. Two underlyings can finish a year at the same price; the leveraged ETFs tracking them can finish that year with very different returns, depending on whether the path was smooth or volatile.

One More Wrinkle: Tracking Error Is a Separate Thing

Volatility decay is the headline story, but it’s worth naming a smaller, separate effect that gets confused with it: tracking error.

Even on a single trading day, a 2× ETF rarely delivers exactly 2× the underlying’s return to the basis point. There are real-world frictions:

- Financing costs. Leverage isn’t free. The fund either borrows to achieve 2× exposure or uses swap contracts that embed a financing cost. That cost drags on returns daily, in small increments.

- Swap spreads and dealer markups. The total return swaps that many leveraged funds use carry costs negotiated with counterparties. Tight, but not zero.

- Rebalance execution slippage. Adjusting the swap notional at each day’s close has small transaction costs.

None of these are decay. They’re operational costs that accrue daily regardless of whether the underlying is volatile or trending. Tracking error explains why a 2× ETF on a flat-volatility day might return 1.98% instead of 2.00%. Small, but separate from the compounding effect that drives multi-day divergence.

What This Means for Holders

The product does exactly what its label says. The label says daily.

Every published prospectus for a 2× daily leveraged ETF makes this explicit. The standard language reads, with minor variations: “The Fund has a daily leveraged investment objective and the Fund’s performance for periods greater than a trading day will be the result of each day’s returns compounded over the period, which is very likely to differ from [2× the underlying’s performance], before fees and expenses.” The math is disclosed. It’s not hidden. It’s just easy to skip past.

The practical implications follow from the math, not from a value judgment about the product:

- The longer the holding period, the more compounded daily returns diverge from a naïve 2× expectation.

- The more volatile the underlying, the larger that divergence, in either direction.

- In a sustained one-way move, leveraged ETFs can outperform their multiple. In a sideways, choppy market, they can underperform substantially.

- The holder’s actual return depends on which regime (trending or choppy) characterized the holding period.

Industry guidance from issuers ranges from “designed for one day or less” (the most conservative framing) to “monitor positions regularly to ensure fund performance aligns with your individual goals” (the more accommodating framing). The SEC’s investor bulletin on leveraged and inverse ETFs notes that these products “are meant to be held for a single day or less.” Whichever guidance you find more useful, the underlying math is the same.

The point of this piece is to make the math visible enough that the choice of how to use these products (for a day, a week, a month, longer) is made with the design in view. The product does what it says. The label says daily. Everything that follows from that is a consequence of compounded returns.

Sources: SEC Office of Investor Education and Advocacy, “Updated Investor Bulletin: Leveraged and Inverse ETFs,” investor.gov. Standard 2× daily leveraged ETF prospectus language regarding daily objective and compounded multi-day performance (representative across issuers). Vol-scaling table: expected return values for a 2× daily-rebalanced ETF on a flat underlying, calculated from the standard daily-rebalanced-leverage formula at the stated annualized volatilities. Hero chart: hypothetical 252-day simulation at 50% annualized volatility with zero drift; underlying simple returns multiplied by 2 for the daily-rebalanced 2× series. Illustrative; not based on any actual fund’s performance.